If you have been in a business owner advisory conversation in the past two or three years, you have almost certainly heard about private credit. Advisors are talking about it. Financial media is covering it. Product manufacturers are packaging it for retail investors. And the returns being quoted — eight, nine, sometimes ten percent — are genuinely eye-catching at a time when a lot of portfolios are searching for income.

But before evaluating any allocation, it is worth understanding what this asset class is, where it came from, and why it grew so fast. The origin story has a great deal to say about the risks. At Avion Wealth, these are conversations we are having with business owners and high-net-worth investors regularly. What follows is the context we consider essential before the yield discussion begins.

A Loan by Another Name

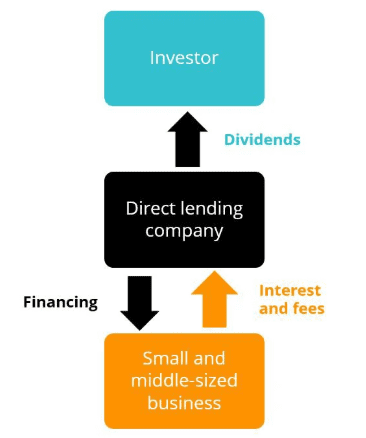

Private credit is, at its most basic level, a loan. A company needs financing. A bank will either not lend to them, or the terms are not attractive. So a non-bank lender — a credit fund, an asset manager, a business development company — steps in and makes that loan directly. The borrower is typically a mid-market company. Not a household name. Not large enough to issue bonds in the public markets. But a real business with real revenue, the kind of company that forms the backbone of the private economy. The lender collects interest on that loan. Investors in the fund receive a share of that income. That is the yield story being quoted.

Two features of this arrangement deserve attention before anything else. First, these loans do not trade on an exchange. They are illiquid. Terms are negotiated privately. Pricing is set privately. Second, the reporting is far less transparent than what investors would encounter in a publicly traded bond or a bank loan. Those two characteristics are not incidental — they are structural, and they carry consequences.

Why Banks Stepped Back

The modern private credit industry is, to a significant degree, a product of the 2008 financial crisis and the regulatory response that followed.

After the crisis, policymakers introduced the Dodd-Frank Act and a series of international capital standards known as Basel III. These rules raised capital requirements for banks and tightened underwriting standards across the board. The practical effect was that making smaller, riskier loans to mid-market companies became economically unattractive for regulated institutions. Community banks, which had historically been the primary capital source for smaller businesses, pulled back further — squeezed by compliance costs that hit smaller institutions disproportionately hard.

Private credit funds stepped into that vacuum. They were not subject to the same regulatory constraints. They could move faster, underwrite more flexibly, and accept risk that banks were no longer willing to carry. The result was dramatic growth. This asset class barely existed at scale before 2008. It now manages approximately two trillion dollars globally — a roughly tenfold increase in fifteen years.

The Economic Contribution: What the Data Shows

It is worth acknowledging that this growth has had real economic benefits. According to a 2024 report commissioned by the American Investment Council, private credit supported approximately 1.6 million jobs in the U.S. economy and contributed around 224 billion dollars to GDP. For business owners in states like Texas, California, and Florida, private credit has been a meaningful source of growth capital in sectors ranging from manufacturing to technology.

This is not a story about a purely extractive industry. For a sustained period, private credit genuinely filled a need the regulated financial system had left unmet. Understanding those benefits, however, is not the same as endorsing the current retail product landscape. That distinction matters, and it is where the conversation becomes more complicated.

What the Origin Story Tells Us About the Risks

The regulatory gap that enabled private credit to grow is the same feature that limits transparency for investors today. Because these funds operate outside the regulatory perimeter that governs banks, they are not subject to the same disclosure requirements. Pricing is infrequent. Valuations are reviewed on a schedule the fund controls. The quality of reporting varies materially across managers.

The regulatory gap that enabled private credit to grow is the same feature that limits transparency for investors today. Because these funds operate outside the regulatory perimeter that governs banks, they are not subject to the same disclosure requirements. Pricing is infrequent. Valuations are reviewed on a schedule the fund controls. The quality of reporting varies materially across managers.

For institutional investors who built their private credit allocations early in the cycle — pension funds, endowments, sovereign wealth funds — these conditions were navigable. They had the resources to conduct deep diligence, relationships with established managers, and entry points from a period when the asset class was less competitive and more generously priced.

The retail product cohort arriving now enters a more mature, more crowded market. The structural considerations facing retail investors in packaged private credit products may include:

- Illiquidity: the underlying loans cannot be sold quickly, and redemption windows may be limited or gated in periods of stress

- Pricing opacity: valuations are set privately and reviewed infrequently, which may mask deterioration

- Fee drag: management and performance fees compress net returns over time

- Timing: retail access has arrived later in the cycle, at higher valuations and with rising default rates emerging in early 2026

None of this renders private credit unsuitable for all investors. It does suggest that the yield figure alone is an incomplete basis for an allocation decision.

The Questions Worth Asking First

Before the yield discussion is the structure discussion. Before the structure discussion is the fit discussion: does this allocation belong in your portfolio at all, at this point in your financial life, in your current tax situation, alongside your other holdings? Those questions do not have universal answers. They have answers that depend on a complete picture of your wealth — not a single asset class evaluated in isolation.

The next post in this series covers what is happening in private credit right now, in early 2026, including the stress signals that are not receiving proportionate attention in the marketing around these products.

For business owners and high-net-worth investors who are currently evaluating private credit exposure, Avion Wealth offers a complimentary second opinion review focused on how alternative allocations may fit within a broader, coordinated wealth strategy.

To your success,

The Avion Wealth Team