Watch the four-minute briefing from Paul Carroll, CEO & Founder of Avion Wealth.

Reports from major commodity traders indicate the global oil market is approaching a critical inflection point. With the Strait of Hormuz blockade now stretching past two months, the inventory cushion that has absorbed the disruption is nearly depleted. By the end of May, crude, gasoline, diesel, and jet fuel stocks may all reach levels at which prices are likely to escalate sharply.

For most consumers, the prospect translates into headlines about prices at the pump. For business owners and high-net-worth families, the more pressing questions are structural. What happens to a wealth plan when the buffer that has cushioned global supply runs out? And how does an existing plan respond once geopolitical conditions normalize?

At Avion Wealth, we treat scenarios of this magnitude as a stress test of existing structures rather than as a forecast to be acted upon. The questions that matter are practical: what may need to be funded from cash rather than from invested assets, where concentrated positions create asymmetric risk, and how recovery is likely to unfold once the immediate disruption ends.

At a Glance

- Global oil stockpiles may reach critically low levels by the end of May 2026 if the blockade in the Strait of Hormuz continues.

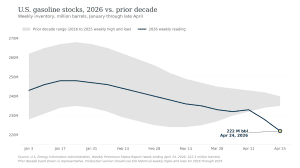

- U.S. gasoline inventories fell to their lowest seasonal level in more than a decade as of late April.

- Energy-sensitive industries and concentrated equity positions deserve a fresh review against the scenario rather than against headline market levels.

- Historical oil shocks suggest economic recovery typically lags the resolution of the underlying disruption by several quarters or longer.

- A complimentary Second Opinion Service is available to families and business owners who want to stress-test an existing wealth strategy.

The Strait of Hormuz and the Stockpile Drawdown

The current condition results from two compounding factors. The blockade in the Strait of Hormuz, now past its second month, has interrupted the flow of a substantial share of seaborne crude exports and global liquefied natural gas trade. At the same time, the inventory buffer that absorbed the initial disruption is being drawn down faster than supply chains can replenish it.

Refineries reprioritized output toward jet fuel and diesel during the early weeks of the disruption, deferring less essential refined products. The U.S. Strategic Petroleum Reserve has been releasing approximately one million barrels per day, slowing the inventory drawdown without preventing it. As of late April, U.S. gasoline stocks reached their lowest seasonal level in more than a decade. The chart below illustrates the pattern.

The summer driving season begins as that cushion runs out. Market participants have cited a wide range of potential price outcomes if the blockade persists, though such projections remain scenario commentary rather than forecasts.

Why Stockpile Levels Matter Beyond the Pump

Energy Information Administration inventory data tends to be discussed in the context of retail gasoline prices. For wealth planning, the relevance runs deeper. Energy is a structural input cost across nearly every sector of the global economy. When stockpiles are tight and prices reset higher, the effect transmits into corporate margins, consumer spending patterns, and central bank decisions on interest rates. Each of those, in turn, has implications for portfolio positioning, business operations, and personal cash flow planning.

The relevance is particularly acute for two groups. The first is business owners whose enterprises consume meaningful energy or rely on transportation-intensive supply chains. A sustained price move can compress margins faster than pricing power can be restored. The second is families with concentrated equity positions, whether in energy-sector companies that may benefit or in industries that may be pressured by higher input costs.

Four Planning Areas to Review in the Current Environment

In an environment of compressing inventory buffers and elevated geopolitical uncertainty, four areas of a wealth plan deserve a fresh review.

1. Liquidity Discipline Before Tactical Positioning

A market dislocation tends to compress both sides of a balance sheet at once. Equity values may decline while bond positions face pressure from rising inflation expectations. Reviewing whether the next twelve to twenty-four months of cash needs are funded from sources that do not require selling into a dislocated market is typically the first item to examine. Tactical positioning in the portfolio is the wrong place to start when the underlying liquidity question has not been answered first.

2. Concentration and Sector Exposure

Direct holdings in energy-sector equities may benefit from a sustained oil price move, while transportation, manufacturing, and consumer discretionary positions may face margin pressure. Concentrated positions, including employer stock, founder shares, and inherited single-stock holdings, deserve review against this scenario specifically rather than against headline market levels. A position that looks reasonable in aggregate may carry meaningful asymmetric risk in a sustained energy shock.

3. Operating Cash Flow for Business Owners

For owners whose revenue or input costs are sensitive to fuel and freight, sustained energy price moves can open a meaningful gap between paper net worth and operating cash flow. Liquidity planning, particularly for owners approaching a sale or transition, may be worth revisiting in coordination with the firm’s existing financial and tax advisors. The valuation conversation looks different when buyers are pricing in uncertainty about input costs.

4. Rebalancing and Tax Coordination

Periods of market dispersion create both rebalancing windows and tax-loss harvesting opportunities. These actions tend to produce better outcomes when executed deliberately, in coordination with existing legal and tax professionals, rather than reactively in response to short-term price action. The objective is to use the dislocation, not to be used by it.

How Past Oil Shocks Have Resolved

The recovery question matters as much as the shock question. Historically, energy-driven economic disruptions have followed a recognizable pattern. Markets price the resolution of the underlying disruption within days. Real economies recover more slowly.

After the 1973 OPEC embargo lifted in March 1974, the U.S. recession persisted into 1975. The full economic recovery took roughly two years from the embargo’s end. After the 1990 Gulf conflict, oil prices normalized within weeks of the resolution, but the broader U.S. slowdown extended into 1991. The 2022 disruption following Russia’s invasion of Ukraine illustrated a different dynamic. Global energy markets rebalanced relatively quickly through redirected supply chains and substitution, while industrial sectors with longer adjustment cycles continued to absorb the shock for several quarters.

The implication for wealth planning is straightforward. A plan that performs adequately during the shock may perform poorly during the recovery if it has been positioned only for the immediate disruption. Both timelines deserve consideration.

A Framework for Stress-Testing a Wealth Plan

The Avion approach to a scenario like this one centers on three structural questions. Whether the plan generates sufficient liquidity from non-portfolio sources to fund the next twenty-four months of obligations without forced sales. Whether concentrated positions are sized appropriately for both the shock case and the recovery case, with explicit consideration of correlated exposures across the household balance sheet. And whether the plan is integrated with the family’s existing legal and tax professionals such that any planning actions taken during a dislocation are also tax-aware and estate-aware.

These questions do not produce a single answer applicable to every situation. What they produce is a framework for examining whether the structure already in place accounts for conditions that differ materially from those in which the plan was originally designed.

Frequently Asked Questions

How does an oil shock typically affect a high-net-worth portfolio?

The effect varies based on portfolio composition, but several patterns recur. Energy-sector equities and certain commodities may benefit, while energy-intensive sectors and consumer discretionary positions may experience margin pressure. Long-duration fixed income may face additional pressure if inflation expectations rise. Diversification and rebalancing discipline tend to determine outcomes more than tactical positioning during the shock itself.

How long do recessions following oil shocks typically last?

Historically, recessions associated with energy-driven inflation have lasted between several quarters and approximately two years. The 1973 to 1975 recession in the United States extended into 1975, and the 1990 to 1991 recession persisted through much of 1991. Recovery patterns vary based on the monetary policy response, the speed of supply normalization, and broader economic conditions at the time of the shock.

Should a wealth plan be adjusted in response to scenarios that have not yet occurred?

Adjustment is rarely the most useful question. Review is. A scenario like a sustained oil shock provides a structured opportunity to examine whether existing plan elements remain appropriate under conditions that differ from those in which the plan was last reviewed. Whether any adjustment is warranted is a determination best made in coordination with the family’s wealth advisor, considering the full picture rather than any single variable.

The Planning Window

The objective is not to predict when the blockade resolves, where Brent crude settles, or how deep any economic slowdown becomes. The objective is to know how a wealth structure would respond if global stockpiles reach critical levels, and how that same structure would respond again as the immediate disruption resolves and the broader economy works through the recovery. Both timelines matter. Both deserve consideration in advance.

For families and business owners who would like to stress-test a current strategy against this scenario or any other, Avion Wealth offers a complimentary Second Opinion Service focused on how an existing plan may hold up under conditions that differ materially from today’s.

To your success,

The Avion Wealth Team

Sources

Ratcliffe, Verity, and Malcolm Moore. “Oil market one month from crunch point as global stockpiles dwindle.” Financial Times, May 1, 2026.