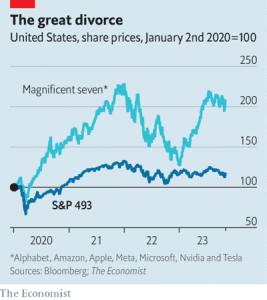

Everybody’s heard of the S&P 500, but maybe what’s more relevant is the S&P 493.

We all consider the S&P 500 to be an important benchmark for investing activities. However, the 493 might be more accurate, and that’s because there are seven stocks, and we call them the Magnificent Seven that significantly distort this index. You’re familiar with these companies, Apple, Microsoft, Amazon, Google, Facebook, or Meta, Tesla, and NVIDIA.  I just read yesterday, NVIDIA’s chips for AI are selling $40,000 for a little chip. So that’s the Magnificent Seven. Valuation wise, they make up 29% of the index, despite only being 1.4% of the 500 stocks, and that’s because the S&P 500 index is what’s known as a cap weighted index. So the Magnificent Seven make up 29% of the value of the index despite only being 1.4% of the stocks. The larger the company, the greater the influence on the index.

I just read yesterday, NVIDIA’s chips for AI are selling $40,000 for a little chip. So that’s the Magnificent Seven. Valuation wise, they make up 29% of the index, despite only being 1.4% of the 500 stocks, and that’s because the S&P 500 index is what’s known as a cap weighted index. So the Magnificent Seven make up 29% of the value of the index despite only being 1.4% of the stocks. The larger the company, the greater the influence on the index.

So if we want a more accurate analysis of what’s going on in the US economy and the true stock market at a broader level, we really need to look at the S&P 493. And what we find is that it’s significantly less volatile. In the crash of 2022, the Magnificent Seven lost 41% of their value, whereas the S&P 493 lost only 12%. There’s a bifurcation in performance here, both on the upside and the downside. We have a seven very volatile stocks that have had an extraordinary run-up since pre COVID. And then we have the 493 stocks that are a better reflection of the US economy.

This outperformance of the Magnificent Seven implies a number of things. It implies that the benchmark is overexposed to a small hot sector of the economy. The Magnificent Seven valuations measured by price earnings and other measures is almost double that of the broader stock market, and that strongly suggests that when the correction occurs, it will be highly focused in that group and relatively painful.

So the lesson of the day isn’t, should we have them, should we be in the index, should we not. It’s beware of the benchmarks, they’re not telling the whole story. And if you are diversified in a manner to better protect you on the downside, then during run-ups, you’re going to feel like you’re being left behind. Of course, the opposite is true when there are market corrections. You’re going to be really glad that you’re not feeling the full brunt of the correction. We wish you the best of investing success.

Sources